Generative Artificial Intelligence (GenAI) is at the heart of major political and strategic discussions across Europe. The European Commission’s Joint Research Centre (JRC) recently released its first-ever Outlook Report on Generative AI, shedding light on the continent’s strengths and weaknesses.

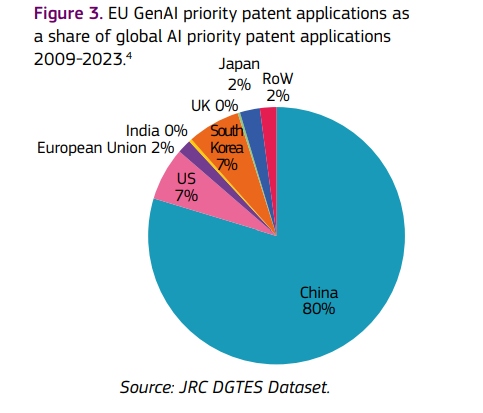

On paper, Europe looks competitive. It ranks second worldwide in academic research on GenAI, demonstrating a robust scientific community driving innovation. However, this research success is yet to translate into commercial power, with EU-based GenAI patent filings accounting for only about two per cent of the global total. This gap highlights a disconnect between academic knowledge and industrial application.

The European Patent Office (EPO) recognises the rapid evolution of AI technologies. According to the EPO, “In recent years, machine learning and AI have been developing at a rapid pace, especially with the advent of large language models and generative AI. EPO is committed to remaining at the forefront of technological innovation. It has responded to the emergence of AI in patent applications, refining its approach to patentability of inventions involving AI.”

EPO is committed to remaining at the forefront of technological innovation and has responded to the emergence of AI in patent applications by refining its approach to patentability of inventions involving AI. – European Patent Office

The European Patent Convention (EPC) excludes computer programs “as such” from patent protection. However, the EPO clarifies that “Software-related inventions can be patentable if they demonstrate a technical character. This means the program must produce a further technical effect beyond the normal interactions with the computer.”

To secure a patent, these inventions must also meet the usual requirements of novelty, inventive step, and industrial applicability.

Funding gaps

Europe’s patent gap is mirrored by a significant venture capital shortfall. GenAI startups in the EU face funding challenges. Compared to US competitors, this limits their ability to scale, attract talent, and commercialise innovations.

European startups and scaleups face persistent obstacles to growth. – Thomas Regnier, spokesperson for DG CONNECT

Thomas Regnier, spokesperson for DG CONNECT, spoke to EU Perspectives about this challenge and recognised that “European startups and scaleups face persistent obstacles to growth due to an incomplete single market, particularly for services and capital, and regulatory fragmentation, including product regulations and standardisation procedures that are out of step with the speed of innovation. They also struggle to obtain adequate financing, especially during their scaleup phase, attract the best talent, or gain access to either public or corporate procurements.”

Technological sovereignty

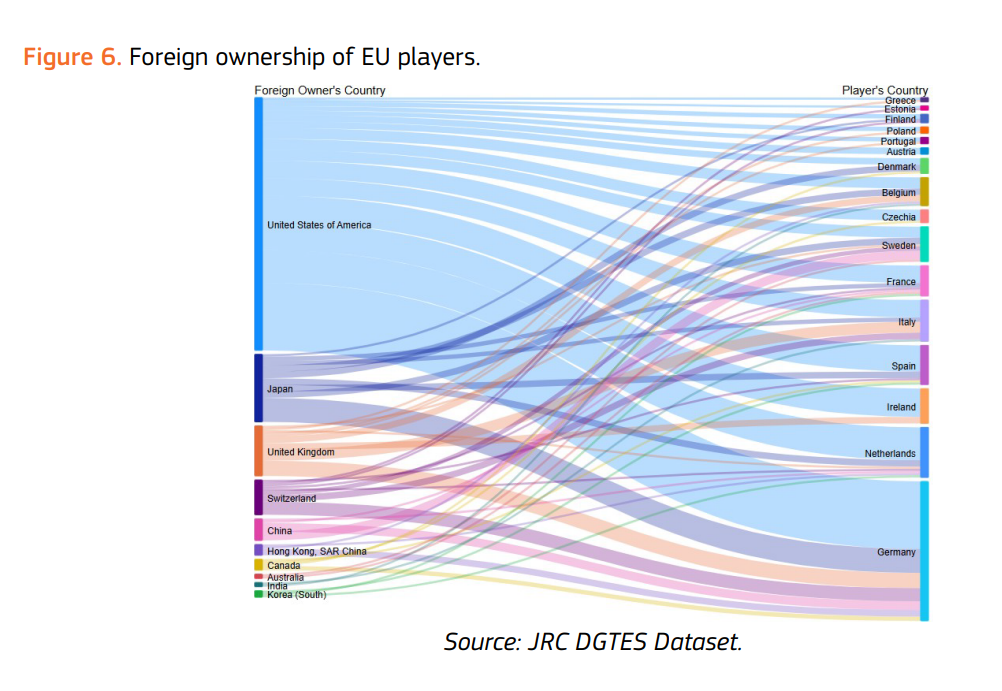

Ownership of GenAI firms within Europe adds complexity. JRC data shows nearly half (49%) of foreign-owned GenAI companies operating in Europe are controlled by U.S. investors. China accounts for five per cent, with Japan and the UK holding 13 and 11 per cent, respectively. Meanwhile, 12 per cent of European GenAI firms are themselves foreign-owned, reflecting a tangled web of international stakes.

The EU holds the second-largest share of foreign-owned GenAI players, signalling investment in GenAI enterprises abroad. Ownership here is defined as a global ultimate owner holding more than 50 per cent of shares of a firm.

Europe is open for business, but only to those who play by our rules. – Thomas Regnier, spokesperson for DG CONNECT

Such opaque ownership arragements raise strategic red flags about how this affects the bloc’s ambition for technological sovereignty. Foreign investment remains important but comes with strings attached. Thomas Regnier, Commission spokesperson for DG CONNECT, stresses: “Europe is open for business, but only to those who play by our rules.”

Europe’s €200bn AI bet

In response, the Commission has launched InvestAI, a €200bn investment programme that includes a €20bn fund for AI gigafactories. These facilities, equipped with roughly 100,000 cutting-edge AI chips, four times more than current factories, aim to anchor Europe’s AI future domestically.

“The AI gigafactories will lead the next wave of frontier AI models and maintain the EU’s strategic autonomy in critical industrial sectors and science, requiring public and private investments.” – Thomas Regnier, spokesperson for DG CONNECT

You might be interested

Europe’s GenAI challenge is to connect that knowledge to markets, close funding gaps, and adapt legal frameworks to the unique demands of AI technologies. Initiatives like InvestAI and GenAI4EU mark important steps forward. Europe’s AI future is a work in progress, and how it will navigate challenges around investment, regulation, and commercialisation will determine its place in the global tech landscape.