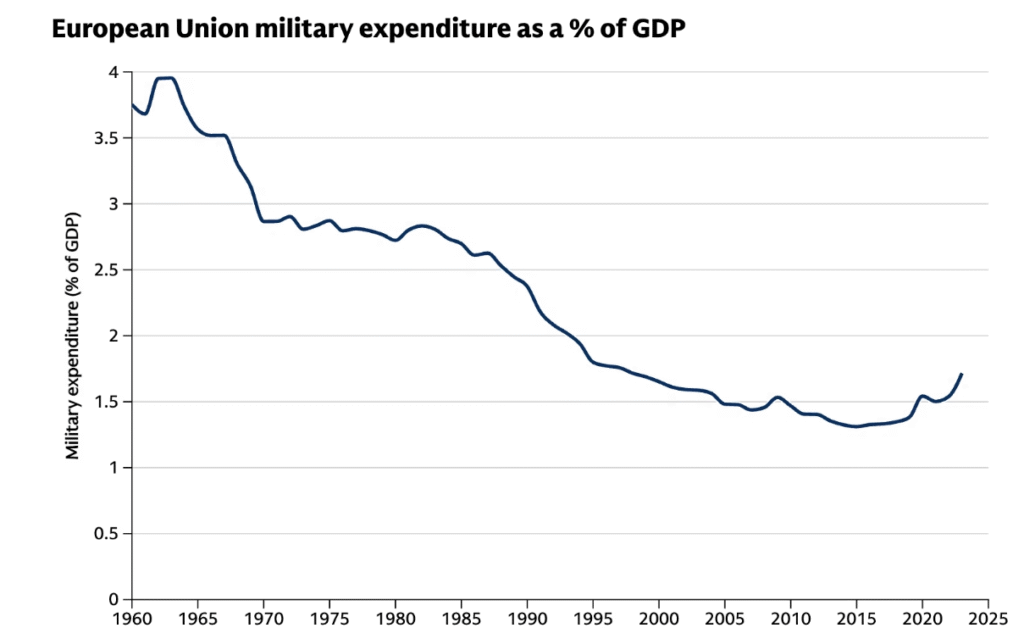

The 1400 Leopard tanks needed to defend Europe would cost less than the German recent batch of 105, if ordered at once. That is why Brussels is weighing a close to a trillion-euro leap from boutique weapon shops to factory-floor barrages. Steel, debt and pooled command will out-gun the Kremlin — if they arrive in time. Now, how do the figures sit together?

Europe’s security environment looks bleak. And the news is? you might ask. Russian ground forces in Ukraine now total about 700,000 troops, backed by annual output of roughly 1,550 tanks, 5,700 armoured vehicles, 450 artillery pieces and 1,800 Lancet loitering munitions. NATO planners used to assume that, if the Baltic states were attacked, the United States would reinforce its 100,000 soldiers already in Europe with as many as 200,000 more.

But with Washington going MAGA, the near-certainty of US involvement is gone. Should the Americans not arrive, the European Union would need an equivalent fighting mass—about 50 heavy brigades, as a minimum. Andrius Kubilius, EU Defence Commissioner, and studies by prominent think-tanks on both side of the Atlantic put the requirement at between 100,000 and 300,000 European troops under a single flag. Other concerns aside, the question is, who is going to pay for it, and how?

Fiscal exceptions

Meeting that goal costs less than most assume. A standing 100,000-strong joint force would need €35-40bn in annual running costs and a one-off capital surge of €45-55bn. That may sound enormous, but in the context of a global geostrategic race for survival, it is but pocket change. Expanding to 300,000 soldiers could doube-to-treble those sums, yet even the ramped-up version of the force adds only 0.75 percentage points to EU defence outlays.

Some of the money is already flowing. Preliminary European Defence Agency data show that members’ real-terms defence spending rose by more than 15 per cent in 2025 and now sits roughly 40 per cent above the 2021 level; equipment investment has almost doubled. Separate figures from the Kiel Institute for the World Economy confirm large procurement programmes in Poland, Germany and the United Kingdom during 2025.

You might be interested

Under the ReArm Europe Plan Brussels has suspended normal fiscal limits, letting governments lift military budgets by up to 1.5 per cent of GDP for four years without triggering an excessive-deficit procedure. The €150bn Security Action for Europe (SAFE) instrument will issue EU bonds and recycle the proceeds as loans provided that 65 per cent of production occurs inside the EU, the EEA-EFTA area or Ukraine.

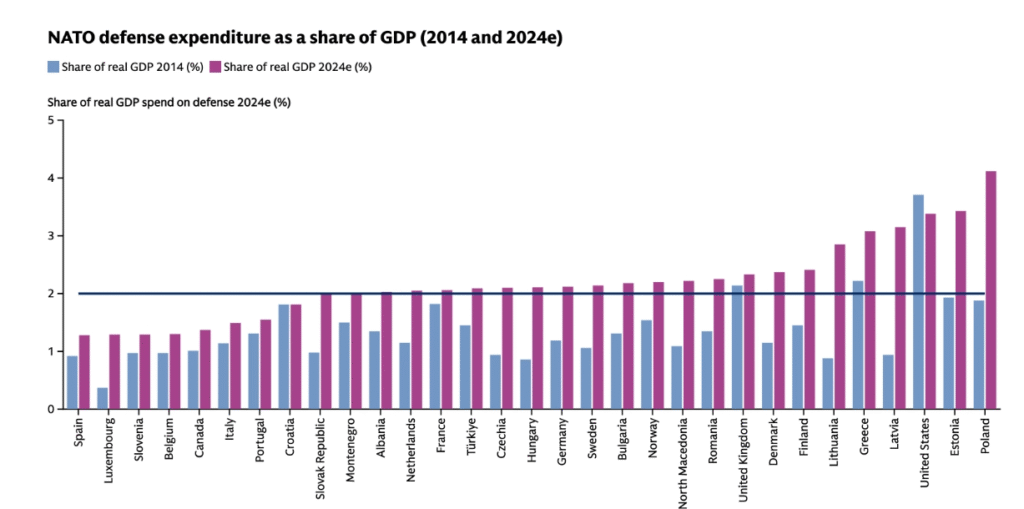

Berlin illustrates the new mood. Germany first met NATO’s two per cent-of-GDP benchmark in 2024 and has amended its constitution so that, in total, about €500bn of extra defence money can be raised by the mid-2030s. This marks an annual increase of just over one per cent of German GDP.

Capability gaps

Structural weaknesses remain. Europe’s 1.47 million active-duty personnel are split among 27 national chains of command, and procurement is fragmented into small batches. Factories still depend on American electronics, Israeli drones and Korean propellants. “This is not primarily a budget problem. European defence spending is rising rapidly. It is a production problem,” The National Interest observes. The US influential bimonthly pinpoints the central challenge: how to build an industrial base that can sustain protracted high-intensity war.

Hardware requirements are steep. To match a single American corps Europe would need about 1,400 modern tanks, 2,000 infantry fighting vehicles and 700 artillery pieces. That is more armour than France, Germany, Italy and Britain together now field. A minimum stockpile of one million 155 mm shells must be held for ninety days of combat, and annual drone output should rise towards 2,000 long-range loiterers. Costs fall sharply when orders are pooled: buying all 1,400 Leopard-class tanks in one bundle would cut the unit price below the €28m Germany paid for its last lot of 105.

Wars are ultimately decided by production, not promises. — Bank of Finland

Five of the world’s twenty largest arms firms are European, and the continent’s automotive and machinery clusters could convert quickly. Yet co-ordination is poor. “GDP percentage is arbitrary mathematics.” The remark comes from last year’s study by the UK’s Tactics Institute for Security and Counter-Terrorism on burden sharing inside the EU-27. It warns that headline targets mask capability gaps unless programmes are unified and standards common.

Debt worse than inflation

Fiscal multipliers show modest macro gains. United States research finds defence-spending multipliers of 0.5-0.8 in normal times; exceptional values of 1.5 were recorded only during the Second World War or the Korean War. In Europe domestic content is lower, the economy is not in recession and interest rates are positive, so expected multipliers are smaller.

Simulations with the IMF’s Global Integrated Monetary and Fiscal Model suggest that a permanent defence rise of one per cent of GDP, financed by borrowing, lifts euro-area GDP in the first year by 0.5–0.9%. Using Europe’s present spending split—70% consumption, 30% investment—the short-run boost is about 0.6%. After ten years the cumulative GDP gain ranges from 0.1% (if all money behaves like consumption, which arguably is a big if) to 1.8% (if it is all investment); the baseline mix gives roughly 0.7%. Ten-year cumulative multipliers run near 1 for investment and about 0.2 for consumption.

Victory depends on industrial endurance, not exquisite platforms. — RAND Corporation

Inflation and interest rates pick up only slightly in the model: both rise by a few tenths of a percentage point. Debt is the bigger concern. A sustained one per cent-of-GDP defence increment adds about nine percentage points to the euro-area debt ratio within a decade. The current fiscal waiver covers 2024-27; permanent spending will stretch rules once that window closes.

Synergies at work

Where money goes matters. Personnel presently absorbs nearly half of European defence budgets, operations and maintenance another 20%, procurement about 30% and R&D less than 5%. In the United States R&D claims roughly 15% of the total. Within European procurement some 60% of orders in 2022 financed traditional platforms—aircraft, ships and vehicles—while emerging technologies attracted far less. Import dependency remains high. Customs data and American export figures show that finished defence-equipment imports equal 10-15% of EU military outlays but more than 30% of equipment procurement (and briefly exceeded 50% in 2017-18). Measured against GDP, imported weapons average 0.10-0.15%.

Nonetheless industry is expanding fast. Turnover is estimated at €110-140bn and employment near 500,000 (as both Aerospace and Defence Industries Association of Europe 2024 and the Draghi report have it). Since January 2022 the market capitalisation of listed European defence firms has almost tripled, against a rise of less than 70 per cent for manufacturing as a whole. Physical output tells a similar story: euro-area production of weapons and ammunition is more than 50 per cent higher than before Russia’s full-scale invasion, and manufacture of ‘other transport equipment‘—a category that includes military vehicles, ships and aircraft—has surged.

GDP percentage is arbitrary mathematics. — Tactics Institute for Security and Counter-Terrorism (UK)

Sectoral linkages are starting to appear. An econometric exercise comparing stock-market returns finds that a 10-percentage-point outperformance by defence shares relative to other industrial stocks precedes a two-year rise of more than three per cent in ammunition output and significant gains in machinery, other transport equipment and electronics. Chemicals, basic metals and electrical gear show little effect, implying that the spill-over is selective rather than broad.

Follow the Poles

The quality of spending can change those dynamics. American programmes that coupled defence orders with civilian technology development have produced long-run multipliers above 2. “Wars are ultimately decided by production, not promises,” says a paper on European defence by the Finland’s central bank. Allocating at least five per cent of every European contract to dual-use R&D would raise spill-overs and help meet civilian innovation goals. SAFE’s 65% domestic-value-added rule pushes in the same direction; preliminary EDA data show that investments now exceed 30% of budgets and R&D rose 18% in 2024. The International Institute for Strategic Studies calculates that equipment plus R&D has climbed from 15% of European NATO budgets in 2014 to 32% in 2024, while the personnel share has fallen from above 60% to about 40%.

Even with better composition, multipliers fade over time. After a decade they fall to 0.1-0.2, debt service rises and private investment risks crowding out. Yet durable structural gains remain possible. A unified European command could save €22bn a year by trimming duplication. The European Defence Fund and the forthcoming European Defence Industry Programme can nurture dual-use research. Professional armed-forces careers can absorb unemployment in regions with slack labour markets.

Recruiting the extra troops will be hard. The average personnel outlay is €140k per soldier per year. Expanding by 300,000 heavy-force soldiers therefore implies a payroll of about €42bn—consistent with Bruegel’s suggestion that aggregate defence outlays might need to rise by €250bn a year in the short term. Poland already channels about 70% of its recent defence increase into equipment. Copying that emphasis elsewhere would trim headquarters fat and improve readiness.

Opportunity costs

Financing options divide opinion. Interest on €125bn of new EU debt each year over five years would cost €27–51bn in two decades—manageable for an economy of €1tn. Spreading the burden across member states reduces moral hazard because capitals that underspend nationally would receive less from common funds. But without durable revenue or an EU-level defence mechanism, debt ratios will keep climbing. “Victory depends on industrial endurance, not exquisite platforms,” a related study by the Rand think-tank stresses.

This is not primarily a budget problem. European defence spending is rising rapidly. It is a production problem. — The National Interest (US)

No analysis is complete without opportunity costs. Input–output tables for Germany, Italy and Spain reveal that €1bn spent on arms yields fewer local jobs than the same amount dedicated to hospitals or schools. Yet the calculus changes when national survival is at stake. “A war economy means something very specific: a permanent industrial posture designed for sustained military production under crisis conditions, with surge capacity built in before, and not after, the shooting intensifies,” a study by the prestigous Munich Personal RePEc Archive claims. Building such posture, needless to say, is cheaper than rebuilding cities reduced to rubble.

Potential trade-offs are manageable. Redirecting €250bn a year to defence could crowd out some green projects, yet the macro cost is modest relative to the devastation of invasion. Short-run GDP gains of roughly 0.6 per cent per extra defence-spending point of GDP are plausible; longer-run benefits depend on whether investment, innovation and domestic supply chains replace today’s personnel-heavy, import-leaky pattern. Public-debt ratios are likely to climb by high single digits over ten years if borrowing does all the work, but that is still below Cold-War US norms.

Policy recommendations

What follows is a distillation of policy recommendations by Aerospace and Defence Industries Association of Europe (ASD), Bank of Finland, Bruegel, International Institute for Strategic Studies (IISS), Kiel Institute for the World Economy, Munich Personal RePEc Archive (MPRA), RAND Corporation, Tactics Institute for Security and Counter-Terrorism (UK), and The National Interest (US).

• Establish a single European command structure by 2027 to remove duplication now costing an estimated €22bn a year

• Ring-fence at least 30% of every defence-budget increase for capital investment and a further 5% for dual-use R&D to push cumulative multipliers towards 1

• Use SAFE loans and EU bonds to fund pooled orders—target 1,400 tanks, 2,000 infantry vehicles and 700 artillery pieces—thereby lowering unit prices below current benchmarks

• Impose a 65% minimum European value-added requirement on all major contracts to contain import leakage now running at 30% of procurement.

Sounds overwhelming? There is more to come.

• Shift personnel growth towards high-skill technical roles; keep average outlay near €140k per soldier to attract mechanics and engineers rather than expand low-skill ranks

• Introduce cost-plus-incentive contracts that reward under-bid performance and penalise overruns, mirroring best practice in the aerospace sector

• Create an EU-level Defence Mechanism to pool debt-service costs and align burden sharing; link disbursements to national spending efforts to curb moral hazard

• Audit procurement every six months—mirroring SAFE practice—and publish comparative dashboards on domestic content, R&D share and delivery timetables

• Accelerate energy and digital-infrastructure reforms to guarantee cheap power and secure cloud services essential for a 300,000-soldier war economy

• Plan for post-2027 fiscal consolidation: commit to gradual revenue measures that stabilise the euro-area debt ratio once the cyclical boost from rearmament wanes.

Damage ahead

Hard choices lie ahead, but the calculus is clear. Europe can fund a joint force large enough to deter Russia for roughly the cost of moving total defence spending to 2.5 per cent of GDP. Multipliers are modest, yet positive if money tilts towards investment and R&D with high domestic content. The alternative—under-investment, reliance on dwindling American reinforcements and fragmented procurement—risks a far greater bill later.

Armaments, not assurances, decide who shapes the continent, the think-tanks say in unison. Europeans take pride in those; but to keep them running, they must also have the real, steel tanks.