With Russian missiles landing near Lviv and Belarus hosting launchers, the European Union is weighing a home-grown nuclear shield. At what cost? The decade-long price of barely 0.11 per cent of GDP a year looks startlingly manageable to economists — particularly in comparison to what the bloc spends elsewhere.

The writing on the wall could not be clearer. Russian President Vladimir Putin rewrote his nuclear playbook in November 2024, warning that Moscow could answer a conventional attack on Russia or Belarus with atomic fire if the attacker enjoyed help from a nuclear power.

Two months later the Kremlin fired an Oreshnik intermediate-range ballistic missile at Ukraine; a second launch in January 2026 landed near Lviv, well within a 5,500-kilometre arc that also covers Reykjavík and Lisbon. Intelligence points to permanent Oreshnik batteries in Belarus and to tests of Burevestnik, a nuclear-powered cruise missile that, in theory, could circle the globe.

No survival outsourcing

Those flashes gave Europe a brutal reminder: conventional rearmament is necessary yet never sufficient when facing over 4,500 Russian warheads. The urgency is too great to ignore. “No great power in history has ever outsourced its survival and survived,” Kaja Kallas, the EU’s top diplomat told the European Defence Agency Annual Conference in January. The strategic debate now turns on a colder question: what would it cost, in euros and industrial disruption, for the European Union to build a credible nuclear shield—its own version of Star Wars, of sorts—of its own?

Consultants who pore over French and British budgets put the headline figure at €200bn–€285bn over the decade 2026-35. That sum folds in €90bn–€135bn of capital procurement for submarines, warheads and command-and-control gear, plus €110bn–€150bn for ten years of operations, maintenance and decommissioning funds. Spread evenly, the bill adds roughly 0.11 per cent of EU GDP a year. The sticker shock is real; the macro-economic dent is modest.

You might be interested

The biggest bite is a fleet of strategic submarines. A six-boat flotilla, scaled from the United Kingdom’s €47bn Dreadnought class, would cost €75bn if built in European yards that already fashion double-hulled tankers and offshore platforms. Warhead design and production—an AWE Aldermaston writ continental—adds €17bn. An airborne leg, perhaps 100 dual-capable Rafales or Gripen-E derivatives, swallows another €10bn. Early-warning satellites, dispersed bunkers and a contingency margin round out the €90bn-€135bn capital range.

Running costs matter. Britain spends about six per cent of its defence budget on the deterrent; applying that rule to projected EU defence outlays gives €110bn–€150bn over ten years. That implies annual cash needs of €15bn–€19bn; money that finance ministers could raise through a mix of SAFE loans, an expanded European Defence Fund and Eurobond issues modelled on pandemic recovery debt. A strategic-autonomy surcharge of 0.05 per cent of gross national income would bring in €7bn a year, enough to pay crews, refuel reactors and keep warheads certified.

A bomb in the balance sheet

Much of this is, however, contingent on the integration of the bloc’s financial markets. The current state of the Savings and Investments Union and the Banking Union, two interconnected Brussels’ flagships projects in the area, is not enouraging.

Even if the burden comes in its lightest possible iteration, it cannot fall on one treasury. Andrea Gilli of Bruegel says that every European NATO member “should pay in line with GDP to stop Spain or Italy free-riding on Poland or Estonia”. Joint borrowing would also avoid breaching the non-proliferation treaty: governments would finance a common programme, not individual bombs.

No great power in history has ever outsourced its survival and survived. — Kaja Kallas, EU High Representative for Foreign Affairs and Security Policy

Indirect economic effects apply as well. Defence firms employed 633,000 Europeans in 2024, up 8.6 per cent on the year. A nuclear build-up would add 45,000-60,000 direct posts and, with a conservative one-to-one multiplier, push total job creation to 90,000–115,000.

Jobs in the dockyard

Shipyards alone would claim a quarter of those gains. Barrow-in-Furness in Britain employs about 6,000 people on the Dreadnought line and sustains a further 17,400 in the supply chain—a 1 : 1.9 ratio. Scale that to a European yard turning out two ballistic-missile submarines a year and 25,000 welders, coders and sonar technicians find work.

Advanced-materials and reactor teams come next. The International Atomic Energy Agency reckons France must recruit 23,000 engineers this decade to keep its civil and military reactors humming. A pan-EU deterrent, with perhaps eight nuclear boats and land-based test loops, pushes that demand to 30,000 physicists, control-rod specialists and metallurgists.

High pay pleases employees — and pinches rivals for talent. Officials fear that draining engineers from offshore wind and battery plants could slow green deployment by 0.2 percentage points for every €10bn shifted to bombs. Sane people would happily pay that price; any guesswork regarding the degree of sanity among European leaders and their voters, however, is well outside the purview of this article.

Spin-offs by design

Supporters counter that dual-use research repays the diversion. France’s CEA-DAM (a division of the French Alternative Energies and Atomic Energy Commission responsible for France’s nukes) has spun off more than 200 firms since 2008. Many of them deal in silicon-carbide cladding, laser machining and 3-D printing. Super-computers built to certify warheads—TERA-100 and its successors—now crunch climate models and quantum-chemistry simulations on their spare cycles.

Navy reactors use compact heat-exchangers and fast-response control software that feed directly into small modular reactors for district heating and hydrogen electrolysers. Compass Lexecon calculates that every €1bn invested in civil nuclear capacity yields €1.3bn–€1.5bn in GDP and about 17,000 jobs.

Future Combat Air System is dead. — Theo Francken, Belgium’s defence minister

Hardened micro-controllers designed for sub-launched ballistic missiles already serve European synthetic-aperture radar satellites. The same gallium-nitride power devices will fly on reusable first stages built by Ariane Group and upstarts in Portugal and Germany.

Squeezing the supply chain

Quantum-resilient communications, another deterrent by-product, guard financial-clearing houses and power grids. By forcing zero-trust architecture—any cybersecurity framework based on the ‘never trust, always verify’ principle—and photonic repeaters into defence networks, the programme subsidises Europe’s late dash to post-quantum encryption.

Warheads devour exotic elements. Europe’s power reactors imported 13,667 t of uranium in 2024; the deterrent would need a few hundred tonnes of highly enriched metal in a decade. Yet enrichment capacity outside Russia is thin. Building fresh cascades costs €0.5bn–€1bn and could nudge uranium spot prices up by five per cent.

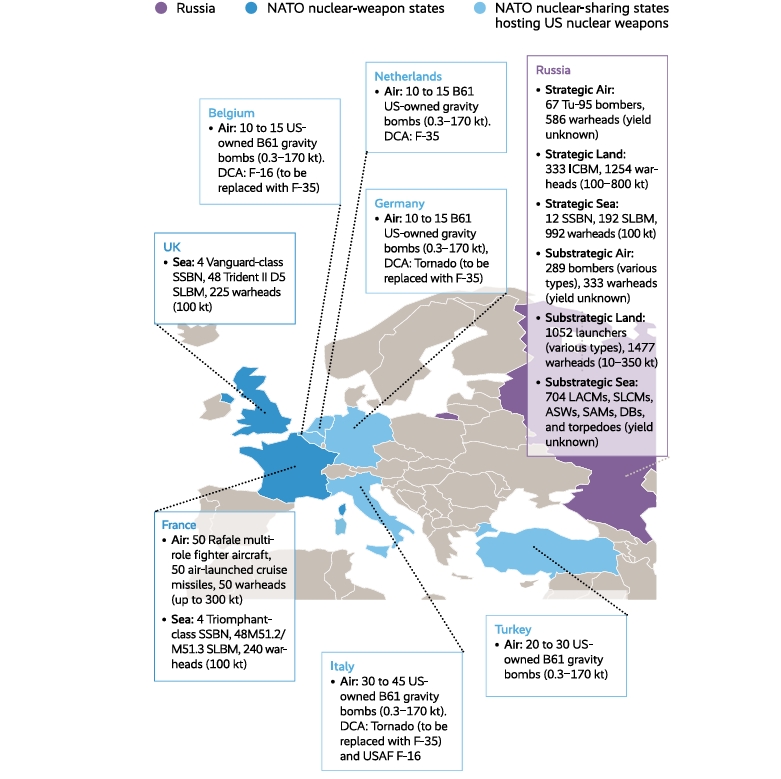

European nuclear capabilites by country

Beryllium, hafnium, tritium and lithium-6 face sharper squeezes. Defence demand may lift prices ten-to-fifteen per cent between 2028 and 2032 unless the EU builds stockpiles, perhaps under Euratom’s existing reserves mandate. Peak construction will coincide with naval and aerospace modernisation, adding an estimated 0.2 percentage points to producer-price inflation.

Commodity strain comes with leverage. A robust home-market for hafnium and rare-earths lets Brussels write longer offtake contracts for mines in Kiruna and Iberia. A credible deterrent may also dissuade coercive cut-offs. (Sabotage of Baltic pipelines in 2022 triggered five-to-ten per cent gas-price spikes.) Lower risk premia could slice €0.2bn–€0.4bn off annual hedging costs for utilities. All these loose ends may well meet in substantial gains.

Learning curves and assembly lines

Economies of scale soften the bill. A Bruegel note reminds readers that “scale economies matter in military production: unit costs are smaller when larger quantities are produced. Weapons production during the WWII increased by a factor of five to ten within a few years, while unit production costs fell dramatically, even after production numbers declined, showing the importance of learning and experience.” The same paper cites Wright’s law, stating that “Unit costs fall by 10 percent to 15 percent for every doubling of aircraft production.”

Europe rarely captures such curves. The Eurofighter Typhoon and Dassault Rafale split burnt billions. Early centralised governance and a single design authority—an Arianespace for deterrence—could avoid a repeat. Scale also helps electronics. The European radiation-hardened micro-controller market, worth €76m in 2025, may climb to €132m by 2035 at six per cent a year if steady submarine orders guarantee fabrication runs in Saxon and Catalan foundries.

Every European NATO member should pay in line with GDP to stop Spain or Italy free-riding on Poland or Estonia. — Andrea Gilli, Bruegel researcher

Unit-cost drops apply to finance as well. Every extra €10bn of Eurobond issuance deepens liquidity, shaves a handful of basis points off coupons and nudges the euro’s share of global oil and gas invoices—now under 20 per cent—towards the 35-40 per cent seen in intra-EU liquefied-gas trades.

Trade-offs on the ledger

Yet opportunity costs endure. Italy and Spain labour under public-debt-to-GDP ratios above 140 per cent; Germany’s debt brake, though bent, still groans. Defence bonds would park liabilities on future taxpayers who may never face a nuclear threat. Mr Merz’s abrupt scrapping of the €100bn Future Combat Air System revealed domestic wariness. “That’s not what we currently need in the German military,” he said. Belgian defence minister Theo Francken put it more bluntly. “FCAS is dead,” he posted on X. (Later this week, the French and German leaders made an attempt at resuscitation, the final result of which is anybody’s guess.)

Political economy intrudes at the local level. Voters near proposed warhead plants fear property de-valuation. British studies of Ministry of Defence sites show house prices falling five-to-ten per cent within 15 km of nuclear facilities. Insurance surcharges follow. Eurozone regulators would need unified compensation rules to prevent lawsuits clogging national courts.

Table: Cost Benchmarking (2026–2035, totals are rounded)

| Building-block | Current national benchmarks | Scaled EU need | Decade cost (€, 2026 prices) |

| SSBN fleet (4–6 boats) | UK Dreadnought programme: €47bn for 4 boats | 4–6 boats + continental basing | 110–75bn |

| Airborne component (dual-capable fighters, ASMP-A/SPEAR-type missiles) | French annual nuclear budget ≈ €5.2bn | Modernise + pool; warhead commonality | 18–25bn |

| Warhead R&D & production (common design) | UK AWE warhead modernisation €17bn over 15 yrs | Shared Franco-German-Italian facility | 12–17bn |

| Strategic C3I & early-warning layer | EU Galileo-PRS + NATO ACCS benchmarks | Hardened sites, satellite upgrades | 5–8bn |

| Infrastructure & security upgrades | NATO nuclear-sharing bases 2000–14 : €202 m | Seven dispersed EU bases | 4–6bn |

| Contingency (20 %) | 17–24bn | ||

| Capital subtotal | ≈ 200–285bn | ||

| 10-yr operating & decommissioning funds (6 % of budget rule-of-thumb) | UK spends ≈6 % of defence budget on deterrent ops | Applied to projected EU-27 defence outlays (€2.2 trn 2026–35) | ≈ 110–150bn |

Still, the deterrent’s macro foot-print is light. Even the top-end €285bn is less than 0.25 per cent of EU output over the decade. The bloc will spend several times that on heat-pump subsidies (the equivalent of rearranging the deck chairs on the Titanic) and semiconductor fabs.

Other factors include sequencing, predictability, and dependency. Delay forces rush orders later, exactly what drove Britain’s Trident overhaul to overrun by €3.45bn. All commerce rewards predictable markets. Lower perceived dependency risk tightens credit spreads for firms that export to volatile regions.

Risk and reward

Economists struggle to price an avoided war, but the benchmark is grim. The first two years of Russia’s assault on Ukraine cut global output by around one per cent. If a home-grown deterrent trims even one-twentieth of the probability of a large European war over twenty years, the expected-loss saving comfortably exceeds the €285bn outlay. That, not jobs in Cherbourg or Barrow, is the core economic argument.

Detractors warn of arms-race spirals. Extra European warheads could spur Russia to mirror moves or tempt China to offer counter-vetoes at the UN. Such blowback would push energy prices higher and erode the strategic-autonomy dividend. For now, however, the more likely risk is European dithering. Each Council summit that ends in a communiqué instead of a bond prospectus lengthens lead times. This is not to be taken lightly: warheads take at least seven years from design to depot; submarine reactors need three years in the forging press alone.

“More is not necessarily better in nuclear deterrence,” a European expert told Reuters, “but France and Britain may still need to increase their arsenal.” Europe must decide whether to do merely that, or to go further and field a fully mutualised shield. The sums are tolerable, the spill-overs tempting and the avoided-war premium incalculable. Yet time, not money, is the scarce resource.

Policy recommendations

The following is a list of policy recommendations compiled from The Economist, Financial Times, European Nuclear Study Group, Fondation pour la recherche stratégique, and Center for International and Security Studies.

- Embed the programme in EU industrial-policy instruments (EDIRPA, Chips Act) to capture spill-overs early.

- Ring-fence at least 30 per cent of project R&D funds for dual-use demonstrators (SMR heat loops, secure satellite buses).

- Use advance-purchase agreements for rad-hard semiconductors to guarantee fabrication runs in European foundries, closing a critical sovereignty gap.

- Coordinate with ECB/ESM to issue green-defence bonds in euros—reinforcing the currency-internationalisation channel while respecting fiscal rules.

Every month of debate, every cancelled aircraft project, every fiscal frown in Berlin pushes the first patrol of a European-flagged ballistic-missile submarine deeper into the 2030s. The strategic logic of self-reliance is harsh; the economic ledger, surprisingly forgiving. What remains is political arithmetic.

The hope is that the current imminent danger gives Europe a unique chance of breaking internal barriers built of national, institutional, and political priorities. The flip side is symmetrical: if it fails, it will suffer uniquely grave consequences. Babylonian king Belshazzar took mene, mene, tekel, upharsin lightly; he was weighed, found wanting, and his empire fell to eastern invaders the same night.