European generals have long complained that more data arrive in headquarters than on the front line. Startups are now trying to flip that balance by beaming, floating, flying and meshing information directly to the units that need it — and much more. A sector once shunned by venture funds has become the continent’s hottest deep-tech bet.

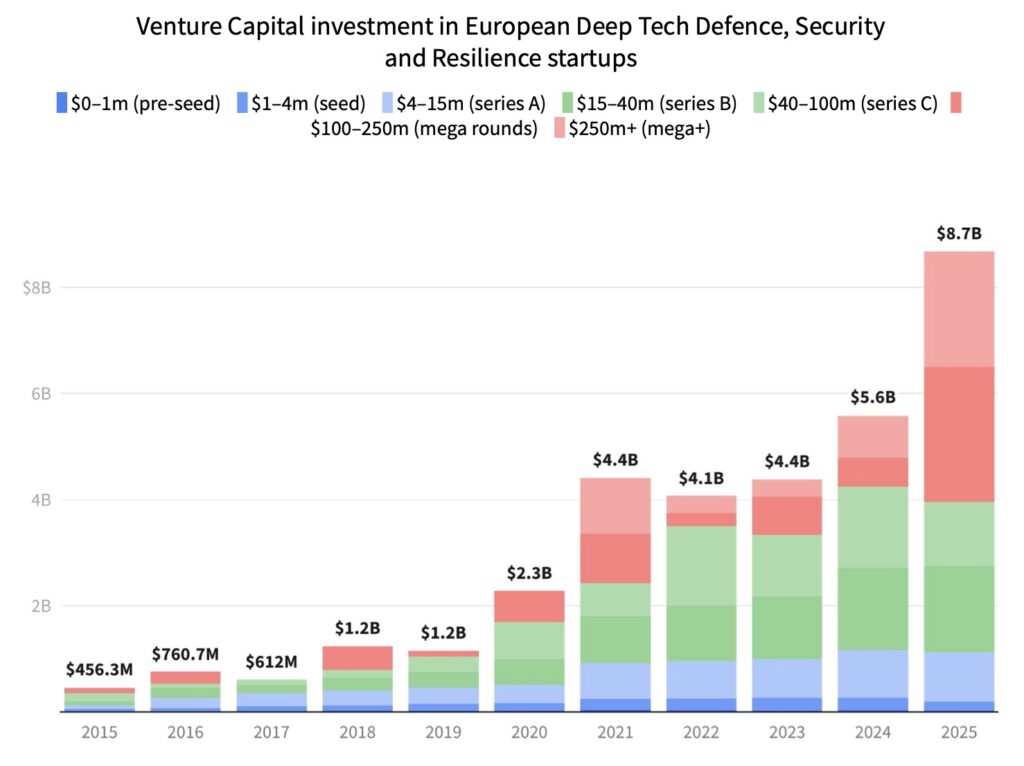

Money talks. Funding for European firms working on defence, security and resilience hit a record €8bn in 2025, up 55 per cent year on year and nearly four times higher than five years ago. Situational awareness, intelligence-surveillance-reconnaissance (ISR) and space systems soaked up 44 per cent of that capital.

The change is visible on factory floors as well as in term sheets. Investors no longer spray cash across dozens of seed bets; instead they pour it into a handful of companies that have cleared the research phase and now need to build hardware at scale. Late-stage rounds tripled to €4.3bn last year, even as early-stage activity paused for breath. Large primes court these newcomers; ministries of defence write contracts rather than merely host demonstrations; all with an eye on accelerating the shift from prototype to deployment.

The Finnish line

That convergence between cash, customers and clear operational needs has turned situational-awareness startups into a full-stack industry. Synthetic-aperture-radar (SAR) satellites feed autonomous drones; edge-computing boxes sift sensor data; ad-hoc networks pipe the results to command posts; decision-support software fuses the lot. The mosaic is still incomplete, but pieces slot together faster than bureaucrats once thought possible.

“Detection and classification of vessels, vehicles, or aircraft will be much easier, which is key in demanding defense and intelligence environments.” That is the leitmotif of ICEYE, a Finnish firm that already operates the world’s largest SAR constellation and intends to keep that lead. In December it raised €150m in a Series E led by General Catalyst.

You might be interested

Rafal Modrzewski, ICEYE’s co-founder and chief executive, spelled out the goal for reporters. “Our team has a strong track record of turning advanced SAR technology into concrete results for customers who need answers in minutes, not days,” he said. “This funding enables us to deepen that commitment by investing in the expansion of our world-leading SAR constellation, next-generation sensing capabilities, and data intelligence services that help governments and organisations manage risk and respond faster.”

The firm’s fourth-generation satellites improve resolution to 16 cm, widen swaths to 400 km and compress data-downlink windows. Sensors that once served mainly insurers and disaster-relief agencies now underpin maritime security in the Baltic and artillery correction in Ukraine. As an ICEYE note put it, “This new generation will empower customers with enhanced situational awareness, faster decision-making capabilities, and improved mission outcomes.” Governments like the speed. Launch contracts on SpaceX rideshares come three at a time.

At the edge of Europe

Data from above still leave gaps below cloud level, particularly in contested airspace where drones draw fire and manned aircraft risk escalation. Janne Hietala, chief executive of Kelluu, thinks hydrogen airships can plug that layer. “We built Kelluu at the edge of Europe, in one of the hardest operating environments outside conflict zones, because we believe that persistent aerial intelligence will become critical infrastructure — not just for defence, but for the resilience of entire countries. That moment has arrived faster than anyone expected.”

Balloons never vanished from military playbooks, but batteries and autonomy now nudge them into a new role. Kelluu’s craft loiter for twelve hours at altitudes below harsh cloud decks, carrying electro-optical, infrared and mapping payloads that stream live feeds to a proprietary platform. The NATO Innovation Fund led its €15m round in January.

Our team has a strong track record of turning advanced SAR technology into concrete results for customers who need answers in minutes, not days.

—Rafal Modrzewski, founder, CEO of ICEYE

Patrick Schneider-Sikorsky, a partner at the fund, liked the range. “Kelluu offers NATO nations persistent, wide-area monitoring and data gathering in challenging environments,” he says. “We are pleased to be backing a company that has built a technology with support from NATO’s DIANA that strengthens the Alliance’s deterrence posture, situational awareness, and resilience.”

New eyes from the east

Central and eastern Europe sit closer to the shooting and therefore innovate faster. Kyiv-based Buntar Aerospace did not exist before Russia’s full-scale invasion; today its Buntar-3 eVTOL drone and Copilot mission-planning software attract €9.6m from backers in Norway and America.

Bohdan Sas, one of the founders, designs alongside brigade commanders. “We build alongside frontline units and understand how important timely intelligence is in real operations,” he told Vestbee, a platform connecting startups and investors. “This financing will help us scale systems that give operators better information sooner and help protect lives in the moments that matter most.”

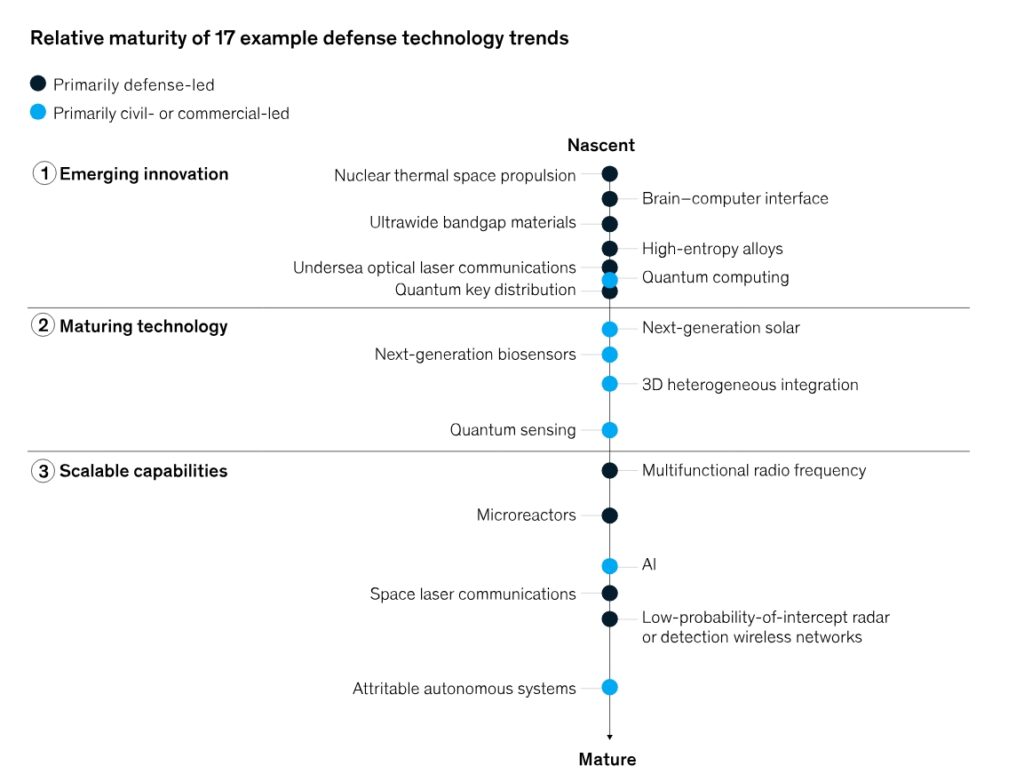

Hardware is only half the job. Copilot uses edge AI to predict flight paths, fuse multi-camera feeds and shrink the time from sensor to shooter. McKinsey, the consulting giant, lumps such computing power into a category called “scalable capabilities”: proven in battle, but not yet adopted at volume because infrastructure and standards lag.

As granular as it gets

Defence AI cannot rely on distant data centres; it must run inside drones, radios, even rifle sights. McKinsey warns that without targeted investment and clear acquisition paths many of the 17 disruptive technologies it tracks could stall.

To reinforce dense but fragile tactical networks, Belgium’s Hiraiwa Defence Solutions offers throw-and-forget mesh nodes the size of grenades. Its Meshed Situational Awareness System forms an auto-healing ad-hoc network that spots armoured columns, friendly patrols and low-flying quadcopters.

For closer encounters the firm’s one-man Battlefield UAV Suppression System jams class-1 and class-2 drones, creating what the founders call a “locally controlled safety dome”. Few Western armies possess enough electronic-warfare teams to accompany every infantry platoon, so portable jammers fill the gap.

Munich rules

Although capital concentrates in Britain and Germany, second-tier hubs mushroom. Munich blends giant primes such as Airbus with robotics institutes and a large pool of automotive engineers.

Dealroom ranks the Bavarian capital as the fastest-growing defence-tech cluster in Europe. The city’s engineers apply automotive supply-chain discipline to space buses and drone frames; investors like the mix (to the tune of €1.7bn last year). Further east the pattern flips: more deals, less money. Polish and Baltic founders close seed rounds quickly but still fly to London or Berlin when they need €50m for a factory.

Some of that late-stage money now flows through tricky structures. Onodrim Industries, based in Amsterdam, skipped angel and seed phases and jumped straight to a €40m first cheque, handling border sensors, multi-domain data fusion and secure networks. The round looked less like venture capital and more like sovereign industrial policy. Governments worry about Chinese or Emirati cash inside critical suppliers and prefer to underwrite equity themselves.

Speed bumps

For all the momentum, three structural hurdles remain. The first is computing power at the edge. Autonomous swarms, LPI/LPD radios and space-based optical links demand accelerated processors that sip, not gulp, watts. Commercial vendors solve the problem with data centres; soldiers cannot drag a warehouse behind them. Defence AI therefore competes with smartphone and automotive firms for the same micro-architectures, driving up costs.

We believe that persistent aerial intelligence will become critical infrastructure — not just for defence, but for the resilience of entire countries.

—Janne Hietala, CEO of Kelluu

Second, newcomers must graft onto brittle legacy systems. Radios bought in 2005 talk one protocol; drones built in 2023 speak another. Standardisation bodies churn, but armies seldom junk perfectly serviceable gear merely to please a startup. Integration contracts thus balloon, and procurement officers delay orders until interoperability proofs appear.

Third, skill shortages bite. A thermal-imaging company in Cologne recently advertised 50 firmware engineering positions and was not able to fill them for months. Wages cannot compete with autonomous-car labs. Some founders try to recruit veterans with coding bootcamps; others lure graduates with stock options and the chance to move at startup speed.

Bridging gaps

Public money looks plentiful but arrives in dribs. McKinsey splits the journey from idea to deployment into three stages. Emerging innovation needs grants; maturing technology needs co-development; scalable capability needs bulk contracts.

Europe covers the first and last stages better than the messy middle. AGILE, a pilot scheme floated by the European Commission this spring, hopes to close that hole by issuing small grants within four months to firms working on urgent operational problems. Total pot: €115m until 2027. Few insiders would consider that sum large, but most praise the tempo.

NATO’s new fund tries to synchronise grant, equity and revenue streams. It can invest in a seed round, invite the firm into DIANA’s accelerator and inject demand signals through allied procurement agencies. The alliance has reviewed 1,300 applications and picked 44 startups so far. Not all work on ISR, but most rely on data flows that eventually end in a command-and-control screen.

A widening front

With no initial public offerings in 2025 (and none in the offing this year), the main exit path remains trade sales. Four times as many mergers and acquisitions closed last year as in 2021. Primes once suspected of smothering innovation now often act as scale-up partners, letting startups bolt their payloads onto established airframes or buying minority stakes. The share-swaps rarely make headlines, but founders say they speed certification and unlock export licences.

Other sectors circle the ISR boom. Quantum-sensor laboratories in Paris work on gravimetric navigation to replace jam-prone GPS. AI-chip startups in Cambridge design neuromorphic processors that run convolutional networks at one watt. Launch providers in Andalusia promise reusable micro-rockets for responsive space. Each fits the broader proposition: Europe can no longer rely on American strategic enablers, so it must build its own stack from orbit to foxhole.

We build alongside frontline units and understand how important timely intelligence is in real operations.

—Bohdan Sas, co-founder of Buntar Aerospace

Governments appear willing to pay. Defence spending across NATO’s European members is likely to top two per cent of GDP this year, releasing tens of billions for procurement. Ministers no longer insist that every euro land inside prime contractors; they carve out budget lines for small suppliers and ask incubators to herd them. Procurement law still hobbles fast deals, but special offices for ‘urgent capability gaps’ proliferate.

Unfinished business

Startups in the situational-awareness niche therefore enjoy tailwinds but face deadlines. Russia produced four million artillery shells last year; Europe two million, as EU Defence Commissioner Andrius Kubilius has grown fond of reminding everyone. Iranian cruise-missile barrages in the Gulf strain American Patriot stocks; allied requests now queue behind replenishment contracts.

Data alone cannot offset such firepower imbalances, yet without real-time picture feeds artillery units waste rounds and air-defence batteries mis-identify targets. Scale will decide whether the current crop becomes integral to Europe’s order of battle or fades into the procurement grey zone. Investors dangle more cash if early customers sign multi-year deals.

The question is whether Europe can build and ship hardware as fast as geopolitical risk compounds. Europe’s situational-awareness startups believe they can. The next two years will show whether ministries of defence and their back-office accountants believe it too — and, more ominously, if it matters.