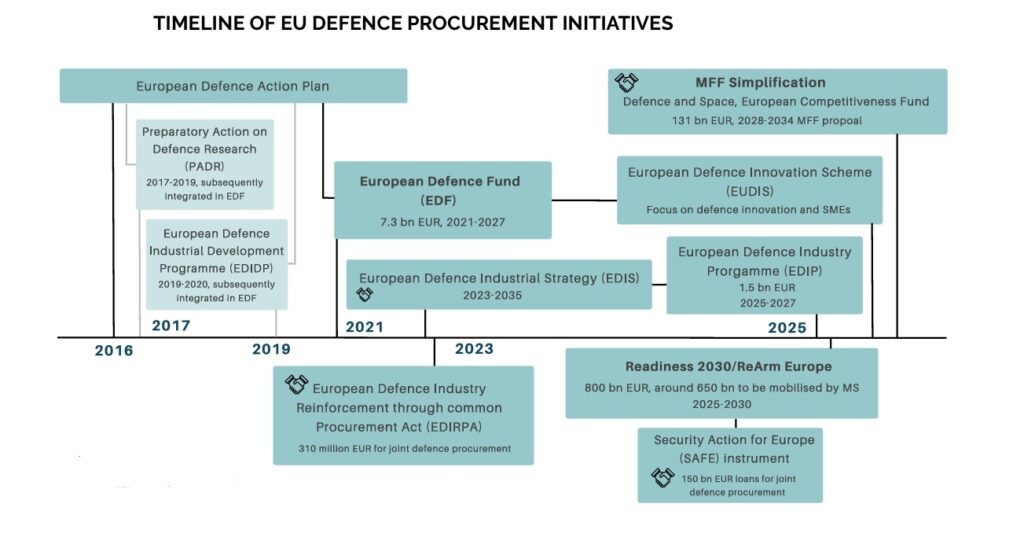

The Union vows to spend more, spend together, and spend European. Yet the cheques it writes tell another story. Roughly €50bn of the €381bn that member states earmarked for defence in 2025 flows to non-EU contractors, chiefly Americans. Closing the gap will be costly—and necessary.

Buy European has a mountain to climb. Europe imported 78 per cent of its urgent defence kit in 2022-23, despite what the slogan claims. Back then, the cost run to €18-57bn a year; that could have funded drone swarms, space sensors and artillery shells.

Things have improved to some 15 per cent last year. But Article 346 of the Treaty on the Functioning of the European Union—allowing governments to bypass normal procurement rules to protect essential security interests—has kept the door open. Defence urgency, industrial gaps and the technological lead enjoyed by a few outside firms push it wide. Lockheed Martin, RTX, Boeing, Northrop Grumman and a pair of Silicon-Valley upstarts sit at the top of the order book.

American eagles

The haul ranges from fifth-generation fighters to anti-drone software. Home-grown champions may complain, but ministries crave kit that works today. Redburn Atlantic, an investment bank, calculates that ‘Buy-European’ caps under the European Defence Industry Reinforcement through Common Procurement Act (EDIRPA) still leave room for 30-40 per cent non-EU content. The Pentagon’s finest exploit every percentile.

Lawyers at Latham & Watkins captured the tension in their thorough February analysis. “Public procurement and standardisation reforms aim to compress timelines and scale output,” they write, before adding that “EU policy promotes a pragmatic ‘European preference’ via lawful levers that emphasise EU origin and control, interoperability, and secure supply”. Brussels wants more local metal yet recognises that it cannot ban imports without hobbling rearmament.

You might be interested

Germany, Poland, Belgium, Greece and others have ordered about 300 F-35s in Lots 18-19, worth roughly €25bn to Lockheed Martin. Berlin alone pays €8bn for 35 jets, including nuclear-sharing certification; Warsaw budgets €6.5bn for 32 aircraft plus €1.2bn for a maintenance hub. Belgium’s €4bn covers 34 fighters, Greece’s €3bn secures 20. Finland, Romania and the Czech Republic add another €8bn between them. Production climbs to 156 aircraft a year in 2026; first European deliveries land in 2027, with operational capability pencilled for 2028.

Why did Eurofighter, Rafale or Gripen not prevail? First, stealth. None of the European types offers the low-observable performance that war-planners crave. Second, certification. Only the F-35 can carry America’s B-61 nuclear bomb, indispensable for Germany’s role in NATO deterrence. Third, scale. Off-the-shelf procurement lets small air forces plug into a global logistics chain, and offsets—Poland enjoys 100 per cent local workshare—sweeten the bill.

Shields up

“Article 101(3) TFEU, the so-called efficiency defence, remains the anchor: Efficiencies must be verifiable, passed on to customers, indispensable, and non-eliminative of competition,” note the Latham lawyers. Ministries brandish that clause to justify single-source deals; speed and commonality outweigh lost competition.

Businesses should form teaming arrangements with clear work-shares and IP, open-interface commitments, and EU ring-fencing for sensitive tech and data.

—Latham & Watkins, European Competition Law and the Defence Industry: Trends, Opportunities, and Risks

Missile defence tells a similar tale. RTX (formerly Raytheon) and MBDA enjoy a €25bn European backlog for Patriot systems. Germany’s slice covers six batteries at €4.5bn plus €1.8bn for Skyceptor interceptors; Poland’s phase-three package totals €12bn for 48 launchers and six IFPC units; Romania, the Netherlands and Sweden together add €3bn for GEM-T missiles. A next-generation project, styled ENG, brings €8bn more across 13 nations, with Lot 1 worth €2.4bn awarded in 2025.

Patriot’s appeal is blunt credibility. Ukraine’s experience shows the system can knock Russian ballistic missiles out of the sky. Diehl’s IRIS-T and MBDA’s Aster work, too, but lack Patriot’s installed base—and its political heft. Production of PAC-3 MSE interceptors will reach 550 a year, promising prompt delivery. The RTX-MBDA joint venture, split 51/49, also slips under EDIRPA’s ownership limits, satisfying the letter if not the spirit of European preference.

Eyes in the sky

“State aid is being applied with urgency to unlock capacity while safeguarding competition,” counsels Latham & Watkins, pointing out that measures “may avoid notification if they protect essential security interests without distorting competition”. Berlin relied on that wiggle room when it fast-tracked Patriot, arguing that ready inventories outweighed the gains from a fresh tender.

Surveillance radars attract fewer headlines than dog-fights, yet they glue coalitions together. Boeing’s E-7 Wedgetail, fitted with Northrop Grumman’s multi-role radar, replaces NATO’s geriatric E-3 AWACS. Britain signed first, paying €2bn for three aircraft; Germany and Italy eye a €1bn trial. NATO budgets €1bn in common funds, while national treasuries cover the rest. Initial capability arrives in 2024 for the Royal Air Force, with alliance deliveries slated for 2029-31.

Boeing also pitches the MQ-28 Loyal Wingman, an autonomous drone developed with Airbus. Demonstrations worth €2bn begin in 2026, hunting a 2030 in-service date. No European airframe matches that maturity; prototypes such as Dassault’s nEUROn remain in flight-test limbo. Saab’s GlobalEye radar plane, under an Airbus marketing deal, offers an indigenous alternative, but defence ministries have yet to bite.

Silicon marauders

Here, too, the legal guardrails prove elastic. The Defence and Sensitive Security Procurement Directive sets competitive rules, yet Article 346 again lets capitals invoke national security. Boeing’s integration with Airbus mollifies critics by sprinkling work inside the bloc and promising open interfaces. Latham & Watkins advise that “businesses should form teaming arrangements with clear work-shares and IP, open-interface commitments, and EU ring-fencing for sensitive tech and data.”

Lockheed and RTX are hardly startups, but the club now includes brash outsiders. Anduril secured a €500m framework with Germany for combat drones and counter-UAS gear running on its Lattice operating system. At least 100 Roadrunner-M interceptors—costing €200m—enter production in 2026, with NATO trials booked for the second quarter. A joint venture with Rheinmetall dodges foreign-content limits by pairing Californian code with Teutonic steel.

Another minnow, Saronic, parlayed a $392m contract with the United States Navy into European attention worth roughly €300m. Norway and Italy plan trials of the firm’s 150-foot autonomous surface vessel in 2026. Sensors, effectors and control algorithms stay American; hulls could be welded locally. European rivals—Naval Group in France, Saildrone in Britain—lag on autonomy.

Startups move fast. Defence ministries, chastened by Ukraine, favour cheap swarming platforms over gold-plated prototypes. Yet even insurgents face Brussels’ bureaucracy. SAFE, a €150bn EU-level lending tool, rewards proposals that, in Latham’s words, “meet eligibility conditions, i.e., EU control of sensitive inputs, interoperable designs, and demonstrable resilience”. Cash flows, but only to those that localise.

Fragmented arsenals

Why can Europe not build at home? Partly, inefficiency. Latham & Watkins diagnose an industry “too fragmented with dominant national players catering mostly to domestic markets”. Small production runs inflate costs; multiyear programmes dribble funding; export approvals splinter. The result, the firm notes, is a “strategic cacophony” that squanders between €18bn and €57bn a year.

“The case for a larger, integrated EU procurement market for defence is well established,”writes the think-tank European Centre for International Political Economy (ECIPE). “Bigger markets deliver sharper competition, lower costs, and stronger incentives for innovation. (…) Europe’s security will not be strengthened by 27 fragmented systems.”

Europe’s security will not be strengthened by 27 fragmented systems.

—ECIPE, Openness and Fragmentation in EU Defence Procurement

Technology gaps widen as primes chase divergent briefs. The Future Combat Air System, a Franco-German-Spanish stealth fighter, will gulp €100bn yet enters service only in 2040. Non-EU suppliers exploit that lull. They promise capability now, backed by American spares. Poland’s defence minister, staring at Russian armour across the border, chose immediacy over ideology.

Money alone will not fix matters. EU industrial policy tries to rewire incentives. SAFE offers cheap loans; the European Investment Bank funnels 3.5 per cent of its 2025 lending—or €3.5bn—into security projects; and the European Investment Fund seeds €175m of equity that should mobilise €500m in private capital. But cash without consolidation merely feeds duplication.

Joining forces

The Commission’s Defence Readiness Roadmap 2030 assigns capability coalitions to missile defence, drones, artillery and other gaps. It also backs four flagships: the European Drone Defence Initiative, Eastern Flank Watch, the European Air Shield and the European Space Shield. Each bundles demand across borders, boosting order volumes and diluting political risk.

Supply-side cures matter as much as pooled demand. Open architectures lower lock-in. Diehl’s IRIS-T launcher now links to Patriot sensors; MBDA’s Aster bolts onto French or Italian radars. Such modularity weakens the one-stop-shop appeal of Lockheed or RTX. If industry standardises interfaces, ministries can mix and match, threatening incumbents with genuine competition.

“Consolidating parties should evidence dynamic competition, supply-chain reinforcement, and speed to scale, and be ready to offer targeted access commitments,” urges Latham & Watkins. Translation: merge smartly, share code when needed, and keep the crown jewels on European soil. EU competition officials nod, so long as open standards curb monopoly rents.

Legal thicket ahead

Foreign-investment screening tightens next. A revised EU regime takes force in 2027, listing artificial intelligence, semiconductors and quantum technology for automatic scrutiny. Transactions already face a maze: the EU Merger Regulation, national security laws and the Foreign Subsidies Regulation overlap. Latham’s caution is crisp. “Investors should plan to align FDI and merger control timetables, anticipate call-ins, and sequence notifications to minimise standstills,” the firm writes. Miss a filing, and factories sit idle.

Even cleared deals may suffer strings. Governments demand governance firewalls, local directors and escrowed source code. Behavioural pledges—say, guaranteed supply to domestic customers—pile compliance costs on outsiders. Some will balk; others will build plants inside the customs union, exactly the localisation Brussels desires.

Time, though, is short. NATO now wants members to spend five per cent of GDP on defence by 2035, with at least 3.5 per cent on core capability. That will flood tender pipelines. If Europe passes the money to outsiders again, its own yards may wither beyond repair.

Closing the gap

Brussels eyes stopgaps. Procurement thresholds under Directive 2009/81/EC will jump to €900,000; a negotiated procedure without prior notice extends to pooled tenders, shaving months. Defence ministers cheer. But without robust industrial contestants the process risks becoming an exercise in faster rubber-stamping for American wares.

Elections loom, too. Populists may baulk at foreign-made fighters while preaching sovereignty. Yet they also fear empty magazines. Firms that embed assembly lines in swing constituencies will thrive. Lockheed’s Polish hub offers a template, churning spares while grooming local engineers. European champions must match such finesse, perhaps by scattering satellite plants across the bloc.

Contractors should maintain auditable EU-content accounting and transparent interface access to support eligibility and evaluation.

—Latham & Watkins, European Competition Law and the Defence Industry: Trends, Opportunities, and Risks

Latham & Watkins warn that “defence financing is expanding, but windows are time-limited” and that “contractors should maintain auditable EU-content accounting and transparent interface access to support eligibility and evaluation.” Compliance departments will therefore matter as much as composite wings. Track every fastener’s origin, open every API, and auditors smile.

For small innovators the hurdles are steeper. Certification costs bite; security clearances stall timelines. Yet mutual recognition clauses offer hope. A start-up that earns German nods may soon ship to Estonia without fresh paperwork. The Commission champions that simplification, betting that nimble firms will fill supply gaps faster than Flag Carriers Inc.

Blueprints for renaissance

Geopolitics may do more than directives. The war in Ukraine reminded leaders that arsenals must be full before crises erupt. Instant procurement favours incumbents with stock and tooling, which today means America. Europeans who lament that fact need to underwrite factories, accelerate testing and pool sovereignty. They might begin by honouring the Commission’s plea to “spend more, spend together, and spend European”.

Until then, non-EU primes will keep cashing cheques. Latham & Watkins conclude that “the evolving policy framework rewards scale, European control of critical inputs, interoperability, and speed of deployment, while maintaining protections on competition and third-country influence.” Washington’s champions tick three of those four boxes already.

Europe’s task is to claim the rest before the next procurement cycle begins. It may pool demand through flagship initiatives, driving batch sizes that justify local lines. Mandating open architectures so new entrants can bolt their widgets onto legacy platforms would surely be helpful. The alternative is as simple as it is unappealing: the EU would have to reconcile itself to renting security from abroad.